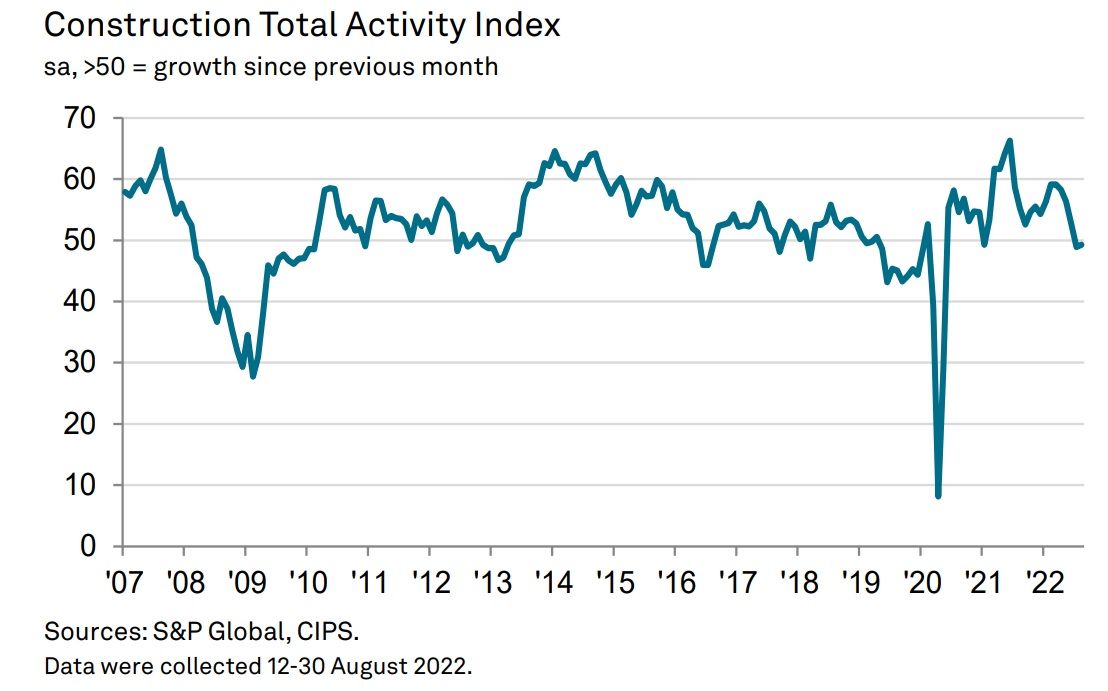

Construction activity in the UK dipped for the second successive month in August as customer demand moved closer to stagnation amid cost pressures and economic uncertainty.

The headline seasonally adjusted S&P Global / CIPS UK Construction Purchasing Managers’ Index (PMI) was at 49.2 in last month, up fractionally from 48.9 in July but still below the 50.0 no-change mark and thus signalling the reduction in construction activity over the month.

As was the case in July, civil engineering posted the sharpest decline in activity of the three monitored categories, seeing output fall markedly over the month. Commercial activity also declined, thereby ending a period of growth stretching back for a year-and-a-half. However, activity on housing projects increased for the first time in three months, albeit fractionally.

Economic concerns

The report also mentioned concerns about wider economic prospects and inflationary pressures led to a drop in business confidence in July and slower job creation, while firms’ purchasing activity declined.

Falling buying activity did alleviate some pressure on supply chains, with lead times lengthening to the least extent in two-and-a-half years in August, while inflationary pressures also showed signs of waning.

Furthermore, in some cases, concerns around the wider economic environment impacted hiring decisions but rising new orders, the clearing of backlogged work and the filling of previously vacant positions kept employment rising solidly, the rate of job creation eased to the softest since March 2021.

In line with the picture for supply-chains, there were also signs of inflationary pressures moderating midway through the third quarter. Input costs continued to increase sharply, often due to higher fuel prices, but the rate of inflation softened to the weakest since February 2021. Similarly, the pace of increase in sub-contractor rates also softened and was the slowest in 16 months.

New orders

While some firms increased activity in response to ongoing growth of new orders, this was outweighed by those constructors that saw output decline as firms adjusted to signs of demand weakening.

New orders increased only marginally in August, and to the least extent since June 2020. Some respondents indicated that customers were holding back on committing to new orders amid cost pressures.

Construction firms scaled back their input buying for the first time since the initial wave of the COVID pandemic, again reflecting signs of a slowdown. There were also some reports that less pronounced price and supply pressures reduced the need to build inventories.

As well as scaling back purchasing and slowing the rate of job creation, construction firms kept their usage of subcontractors unchanged in August. This ended an 18-month sequence of expansion. Meanwhile, the rate of subcontractor availability continued to fall sharply, and to the largest degree in six months.

{kind=link}