Recovery in UK construction output lost momentum in July, with contractors struggling to keep up with the surge in demand for construction projects due to raw material supply shortages and shrinking subcontractor availability.

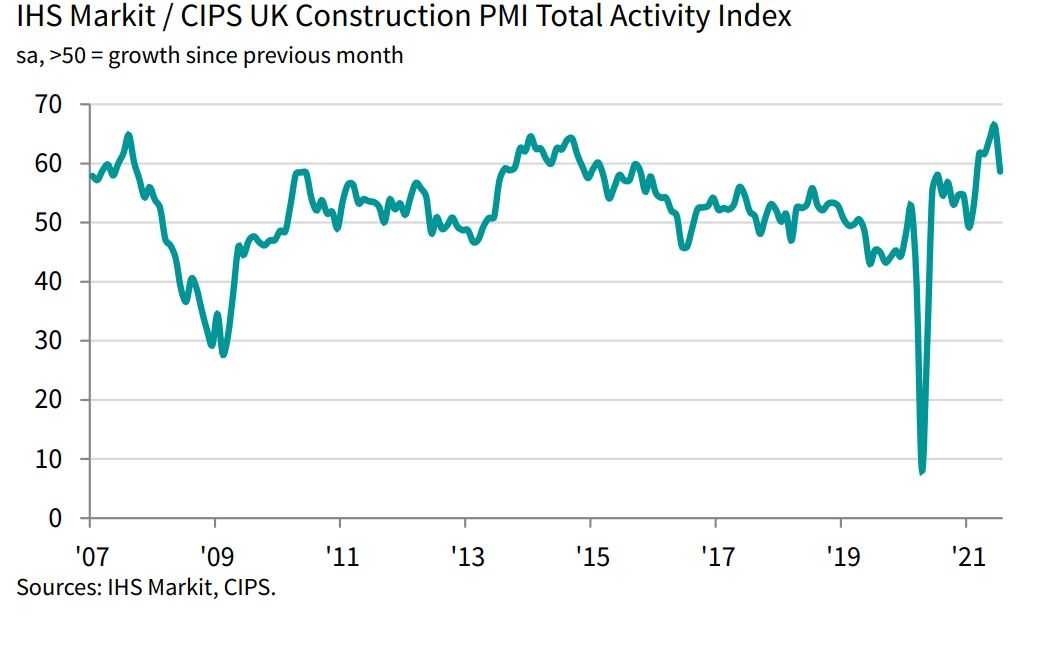

The headline seasonally adjusted IHS Markit/CIPS UK Construction PMI Total Activity Index registered 58.7 in July, down sharply from June’s 24-year high of 66.3, but still well above the crucial 50.0 no-change threshold. This latest reading signalled the slowest overall increase in construction output since February.

The July PMI data highlighted that slower growth had been seen in all three main categories of work. The latest data also signalled another steep increase in purchasing prices, with around 81% of the survey panel reporting a rise in their average cost burdens during July, while only 1% signalled a decline.

However, total order books continued to improve in July, but the latest rise in new work was the weakest since March. Similarly, input buying expanded at the slowest pace since April amid a softer recovery in demand. Construction companies also noted that reduced materials availability had acted as a brake on purchasing volumes in July.

Shortage and supply issues

Around 66% of the survey panel reported longer wait times for supplier deliveries in July, while only 2% signalled an improvement in vendor performance. The resulting index signalled widespread supply chain delays, although the latest reading was up from June’s record low and the highest for three months. Survey respondents noted that supply imbalances were amplified by a lack of transport availability, port congestion, and Brexit trade frictions.

A rapid pace of input cost inflation continued in July, fuelled by supply shortages and robust demand for construction items. Higher charges among sub-contractors and difficulties filling staff vacancies also added to price pressures.

The latest decline in sub-contractor availability was the second-fastest since the survey began in 1997, exceeded only by that seen during the lockdown in April 2020.

However, construction firms continued to hire staff at a strong pace, reflecting rising orders and confidence regarding the near-term outlook. While optimism toward future output growth remained historically high, the index drifted down to its lowest for six months in July.

Housebuilding

Housebuilding was the best-performing category in July (index at 60.3), followed closely by commercial building (59.2). In both cases, the rate of expansion was the weakest since February. This mostly reflected stretched business capacity and growth constraints due to supply issues, but some firms noted that the post-lockdown spike in customer demand had started to wane.

Civil engineering

Civil engineering activity (55.0) followed the momentum seen elsewhere in the construction sector during July, with growth easing sharply since June and the lowest for five months.

Commenting on the latest figures, Matthew Farrow, director of policy at the Association for Consultancy and Engineering, said: “Despite the difficult circumstances the industry is collectively facing, overall trends are still positive. However, it is also clear that the ‘perfect storm’ of Brexit trading delays, global supply pressures, and COVID, is now severely impacting on construction in the UK.

“The industry needs to continue to work together, through forums like the Construction Leadership Council, if it is to lessen the impact of these structural issues in the coming months. This is the only way to avoid the stalling of strong post-pandemic growth.”

{kind=link}