Construction activity continued throughout the first quarter of 2021, and double-digit growth is forecast this year, according to the Construction Product Association’s (CPA) latest Spring Forecast published on 26 April.

Activity was not hit as hard compared to the first lockdown in 2020, thanks to the whole supply chain (architects, consultants, contractors, small to medium-sized enterprises, manufacturers and merchants) being permitted to operate during the winter lockdown restrictions.

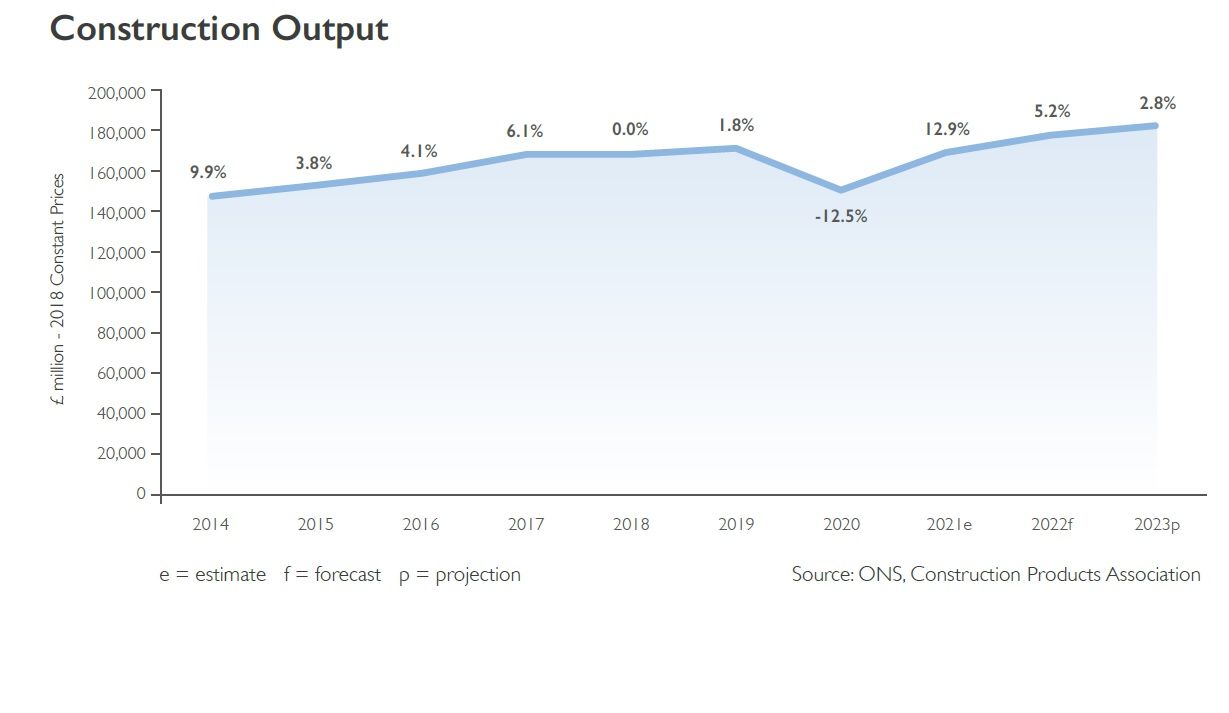

However, the CPA forecasts that it will be next year before the industry recovers the output lost in 2020 and returns to 2019 levels. It also highlights significant risks to the construction sector’s recovery from 2021, including supply constraints for key imported construction products and uncertainty around demand for housing newbuilds, repair, maintenance and improvements works (RMI), and commercial space.

Rising output

Construction output is forecast to rise by 12.9% in 2021 and 5.2% in 2022 compared with 14.0% in 2021 and 4.9% in 2022 in the CPA’s winter main scenario. The downward revision to the growth forecast for 2021 reflects a higher base for construction output in 2020, with official data reporting a smaller fall than initially anticipated of 12.5% in 2020 compared to 2019.

The UK economy faltered in 2021 Q1 due to the impacts of the third national lockdown on the services sector that accounts for 81% of UK GDP. However, for construction, activity accelerated in the first quarter of the year.

Infrastructure was least affected by the initial lockdown as it was considerably easier to enact site operating procedures and other safety measures on large sites. In 2021, output is set to increase by 29.3%, reaching its highest level on record. This will be driven by activity on major projects such as HS2, despite the announcement of further delays and cost overruns, as well as activity on long-term frameworks in regulated sectors such as water, roads, electricity and broadband.

Sustaining demand

Furthermore, extensions to the stamp duty holiday, Help to Buy and job support schemes are expected to help sustain demand in private housing and private housing RMI.

Private housing, which was the worst-affected construction sector in the initial lockdown is expected to continue its strong recovery in 2021, with the Chancellor’s ‘Mortgage Guarantee Scheme’ likely to enable demand in the general housing market.

Coupled with expectations of rising house prices during the year, starts activity is forecast to gather pace in 2022. Additionally, demand for contracted-out improvement projects, outdoor and office-related space requirements at home is likely to be maintained by households with higher incomes and those that have built up savings due to a reduction in commuting and work-related expenses.

A word from Noble Francis

Commenting on the Spring Forecast, Noble Francis, economics director at the CPA, said: “Whilst outlook is largely positive, the recovery in commercial – the third-largest construction sector – is expected to be muted given a lack of major investment in new projects, particularly in central London.

“Questions remain over future demand of commercial space, particularly in offices and retail, which may be converted into residential or warehousing and logistics, if homeworking and online spending persists in the long-term.

“More notably, however, there are significant risks to the recovery in the form of supply constraints in terms of extended lead times and sharp rises in costs for vital imported products such as paints and varnishes, timber, roofing materials, copper, steel and polymers. This may hinder the ability of construction activity to increase in line with our forecast.

“Furthermore, concerns remain whether the high levels of demand for housing newbuild and RMI can be maintained after the government stimulus and policy measures end on 30 September, particularly the furloughing and self-employment income schemes and stamp duty holiday.”

{kind=link}