The construction sector saw a return to growth in September after two months of falling output, but business optimism reached its lowest since July 2020 as new orders stalled.

The latest UK Construction PMI data reported that survey respondents remain cautious about their growth prospects looking ahead to the next 12 months. Despite the growth in September, the drop in business optimism reflected concerns about higher interest rates and a downturn in the wider UK economy. However, supply shortages eased in September, with delivery delays the least widespread since February 2020.

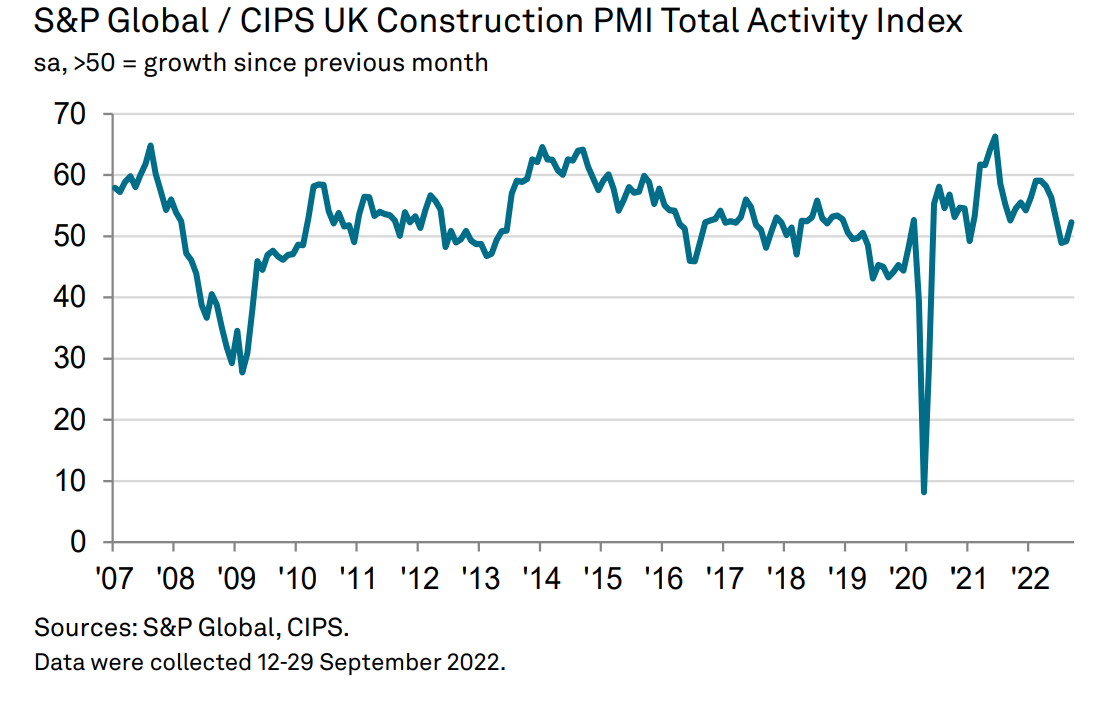

Purchasing Managers’ Index (PMI)

The headline seasonally adjusted S&P Global / CIPS UK Construction Purchasing Managers’ Index® (PMI®) was at 52.3 in September, up from 49.2 in August, registering above the 50.0 no-change value for the first time since June. Considering the growth in construction output, survey respondents commented on a boost to activity from work on previously delayed projects and outstanding work, but incoming new orders remained relatively scarce in September.

House building was the best-performing category in September (index at 52.9), with growth reaching a five-month high. Commercial work increased only marginally (51.0), while civil engineering activity (49.6) fell for the third month in a row.

New orders

Latest data signalled that new business volumes were broadly unchanged overall, which represented the worst month for new orders for almost two and-a-half years. Construction firms cited slow decision making among clients and greater risk aversion due to inflation concerns, squeezed budgets and worries about the economic outlook.

Subdued client demand contributed to a marginal reduction in purchasing activity across the construction sector. Survey respondents also suggested that a turnaround in supplier performance had led to reduced inventory building. Latest data signalled the least marked lengthening of vendor lead times since the pandemic began.

Jobs

Employment growth accelerated from August’s 17-month low. Around 21% of the survey panel reported a rise in staffing levels, while only 8% signalled a decline. Higher workforce numbers reflected efforts to boost business capacity, although construction firms continued to cite shortages of candidates to fill vacancies and strong wage pressures.

Inflation

Average cost burdens increased sharply in September, but the overall rate of inflation eased to its lowest since February 2021. Survey respondents noted escalating energy costs and greater prices paid across the board for construction products and materials. Lower fuel prices and improved transportation availability were cited as factors helping to moderate the overall pace of cost inflation in September.

Industry reaction

Brendan Sharkey, head of construction and real estate at MHA, says that despite the sector’s continued growth, the hike in interest rates and spiralling mortgage crisis threatens the sector’s property market continued success.

He said: “Despite the cost of living and energy crisis gripping the country, the construction sector has of late coped with inflationary pressures by adjusting prices to maintain margins. While the economic landscape, coupled with the falling value of the pound, may deter UK investors in the immediate term, thereby impacting on future projects and slowing productivity, there is no slowdown of work for the sector as it stands.

“For the housing market, demand continues to remain strong however this will undoubtedly dip in the months ahead. The mortgage crisis following the Bank of England raising interest rates to 2.25% eliminates any economic benefits gained through the reduced stamp duty rate. Ultimately, it creates zero incentive for homeowners to move or buy and potentially limits the ability and appetite of first time buyers from getting on the property ladder. Property prices should stabilise at best, but if employment falls expect to see falling prices.

“Last week’s mini-budget failed to produce any clear policies that provide additional support for the sector, meaning businesses face an uncertain future. The introduction of Investment Zones, while designed to stimulate economic activity and housing development within local economies, lacks sufficient detail on how the zones would work, the planning details required and the approval process. As a minimum the government must address these points to enable the sector to fully grasp the opportunities it will present.

“The government should reintroduce tax relief on mortgage interest for first-time buyers to stimulate the property market. This relief would run alongside the first-time buyers stamp duty reduction making an attractive incentive to both the buyer and developer. Ultimately, the government must deliver their promises on time, without delays and with clarity to ensure that activity within the construction sector continues to flourish.”

Meanwhile, Toby Banfield, restructuring partner at PwC said: “While the latest PMI shows sector growth and easing supply shortages in September, a deeper dive reveals ongoing pressure with the weakest trend for new orders since June 2020 and overall confidence dropping to its lowest for over two years.

“Construction contracts are typically cash positive from a working capital perspective which means customers pay up front for various phases of work before the construction starts. A drop in new project volumes reduces cash coming into the business, which is leading to cash flow challenges for businesses – a move that is increasing pressure with previous cash receipts already used to meet unexpected material price increases on existing projects.

“Getting costs under control, doing proper bottom up forecasts and locking in as many variable costs as possible, with hedging or inflation options will all be critical for managing cash flow going forwards. The manner in which firms react could make all the difference over the next few months.”

Paul Sloman, PwC engineering and construction leader, added his perspective on the PMI results: “In the energy-intensive construction sector, businesses will still come under pressure to build up their inventories to protect against supplier delays. There will also be a focus on cutting costs, as it becomes darker and chillier, just as heat, power and lighting bills rise from October.

“Preserving cash, getting their forecasting in order and finding ways to return input material costs to previous levels is a major priority.

“Even where the government has decisively stepped in, with measures like the corporate energy price guarantee, costs are still rising. We estimate October energy contract renewals will still lead to at least a doubling in prices in many cases.”

{kind=link}