Building companies have seen the fastest rise in construction output for eight months, with the latest PMI data suggesting that business activity gained momentum across the UK construction sector in February.

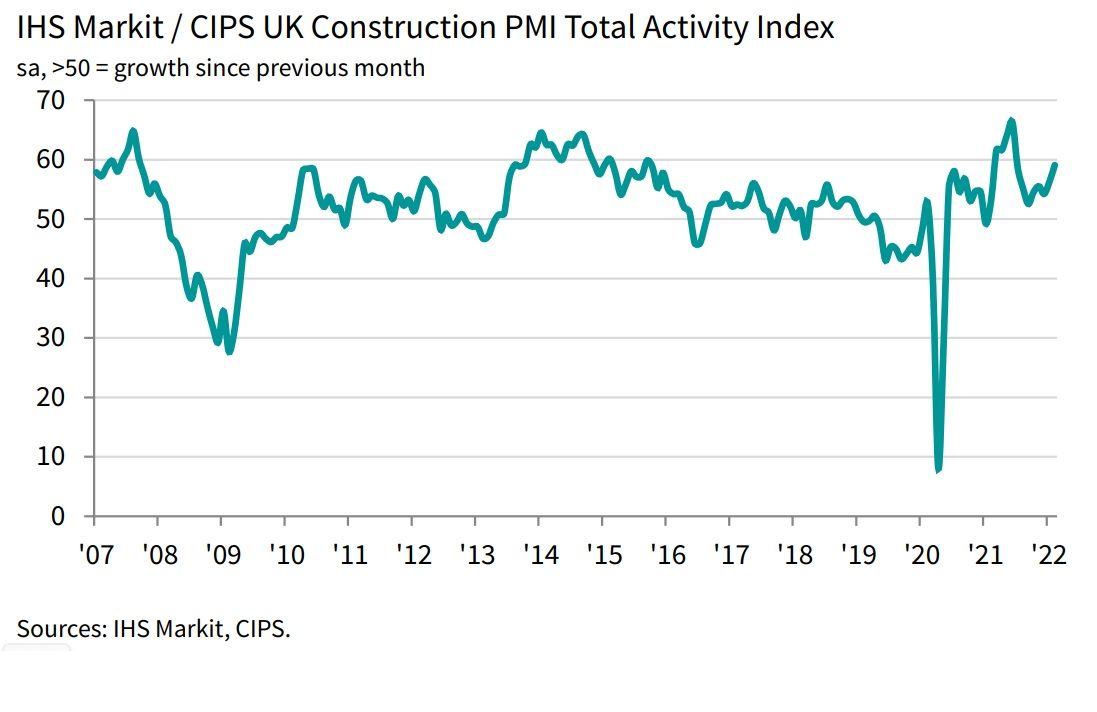

The headline seasonally adjusted IHS Markit/CIPS UK Construction PMI Total Activity Index registered 59.1 in February 2022, up from 56.3 in January, signalling a robust and accelerated rise in output volumes. The headline index has now posted above the neutral 50.0 threshold in each of the last 13 months.

However, construction companies continued to report widespread supply constraints – which has put confidence at its lowest since January 2021 and dampened the year ahead outlook – and rapidly increasing input costs, though the rate of inflation in the latter was the least severe for 11 months.

Index breakdown

House building (index at 61.5) replaced commercial work (58.4) as the best performing category of construction work in February. The latest increase in residential work was the strongest for eight months. Commercial construction also expanded at a quicker pace than in January, with the rate of growth the sharpest since last July. Meanwhile, civil engineering activity (index at 57.5) increased at an accelerated pace that was the strongest since June 2021.

New order growth accelerated for the fourth month running in the latest survey period to extend the current sequence of expansion to 21 months. Moreover, the rate of growth was the fastest since last August as construction companies commented on stronger client demand in line with the recovery in economic activity and new projects being brought to tender.

Resilient pipelines of new work were highlighted by a steep rise in input buying across the construction sector during February. The latest expansion was the fastest for seven months and commonly reflected pre-purchasing ahead of new project starts. Staffing levels also increased at a sharp pace, extending the sequence of job creation to 13 months.

Rising input prices

The latest data also signalled another rapid rise in input prices, though the rate of inflation eased to an 11-month low. The increase in purchase prices was often attributed to rising raw material and commodity prices amid supply shortages, alongside a lack of transport capacity.

Longer delivery times

Around 36% of the survey panel reported longer delivery times among suppliers in February, while only 4% saw an improvement. Delays were overwhelmingly linked to ongoing driver and material shortages, as well as international shipping delays. However, the number of construction firms reporting longer lead times for deliveries was down from a peak of 77% in mid-2021.

Future outlook

Overall, the near-term outlook for construction activity remained positive in February. Just under half of the survey panel (48%) forecast an increase in output during the year ahead, while only 9% predicted a fall. However, the overall degree of optimism eased to the softest since January 2021 as firms cited concerns about the impact of rising costs and supply shortages.

Industry thoughts

Following the release, Brendan Sharkey, head of construction and real estate at MHA, says the UK housing market is still very strong and Brexit has already prepared the sector for possible supply chain disruption arising from Russia’s invasion of Ukraine: “The UK construction sector has got a good wind in its sails. Inflation is a very grave concern but there are real strengths underpinning demand for new-build housing. In addition, we’re starting to see that Brexit, although painful, has already led to businesses in the sector diversifying their supply chains. This stands them in good stead to weather the economic shocks of Russia’s invasion of the Ukraine.

“Housing demand shows little sign of seriously slowing. In the end, it turns out that Stamp Duty relief (which has ended) and even possibly Help to Buy were not necessary to buoy the market. Two big factors explain the current very high demand for new housing. First, renting is getting ever more expensive, so it makes sense for people to get on the housing ladder, while mortgage rates are still reasonable, even though house prices are high. Second, energy efficiency regulations are driving buyers, investors and developers towards new-builds because older homes usually don’t meet the requirements.

“However, inflation remains a real menace. The ultimate cause of the kind of inflation the sector dreads is the rising price of energy with oil and liquefied natural gas (LNG) prices now sky high. As margins are thin in the construction sector, there is a real prospect inflationary pressures, without proper controls, will put an end to some businesses.

“Brexit was a trauma for the sector, but people have now adapted to an extent to the new environment. Businesses are paying more attention to their supply chains and understand the need for diversification more than they did. This means the sector might be slightly better placed to weather disruption flowing from the Russian invasion of Ukraine than it would have been had Brexit not happened.”

>>Read more about the sector’s performance here.

{kind=link}