Sales figures for Q4 2022 in the Builders Merchants Federation’s (BMF) Builders Merchants Building Index (BMBI) has shown signs of a slowdown.

Q4 2022 v Q3 2022

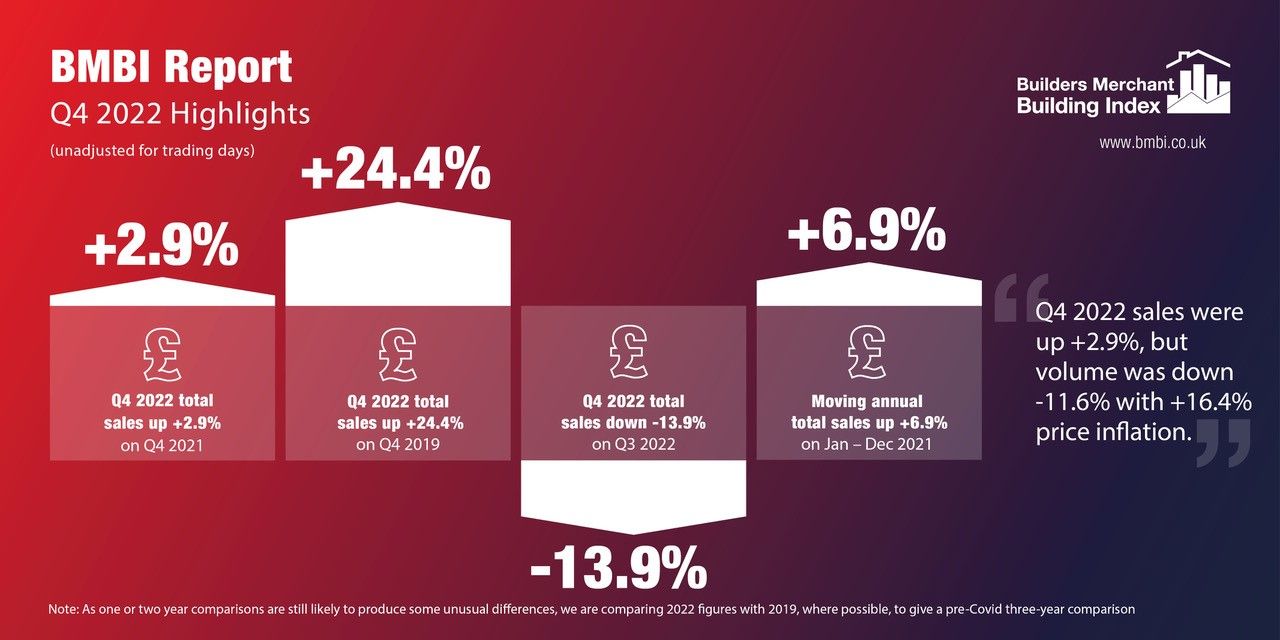

Total sales values in Q4 were -13.9% lower than in Q3 2022, with volume sales dropping by -18.3%, but prices increased by +5.4%. With five less trading days in Q4, like-for-like sales values, adjusted for the difference in trading days, were down by -6.6% .

Only three smaller product categories recorded an increase in sales value, one including Workwear & Safetywear, which grew by +7.1%

The largest two product categories both recorded double digit falls, with Heavy Building Materials down by -13.7% and Timber & Joinery down by -16.6%. The seasonal category of Landscaping saw the largest fall as -33.6%.

Q4 2022 v Q4 2021

Total sales in Q4 2022 were up by +2.9% on Q4 2021, but this was largely price driven with volume sales down by -11.6% and prices up by +16.4%. Adjusted for one less trading day in 2022, like-for-like sales were +4.6% higher.

Ten of the twelve categories saw sales values increase year on year, led by Renewables & Water Saving (+48.6%). Plumbing, Heating & Electrical (+18.6%) and Workwear & Safetywear (+14.8%) had their highest quarter revenue and were among categories which grew faster than Merchants overall such as Heavy Building Materials, which increased by +8.6%.

Landscaping (-5.9%) and Timber & Joinery Products (-11.5%) were the only categories to sell less in Q4 2022 over Q4 2021.

2022 vs 2021

Across the full year the builders merchants sector saw value growth against 2021 of +6.9%, driven by price growth of +16.2% and a volume decline of -8.0%. With three less trading days in 2022, overall like-for-like sales were +8.2% higher.

All categories saw value growth apart from Timber & Joinery, which was down by -2.2%, and Landscaping, which was down by -0.6%.

The best performing category was Renewables and Water Management at +31.5%, followed by Kitchens & Bathrooms (+18.9%), and Plumbing, Heating & Electrical (+14.8).

For Heavy Building Materials, the full year saw a value increase of +11.6% with a noticeable price growth of +18.6%. Volume was down by -5.9% indicating that it was less affected than Timber & Joinery, which saw volume declines of -15.5%.

Commenting on the report John Newcomb, CEO of the BMF, said: “With so much volatility in the UK economy in 2022, it comes as no surprise to see the slowdown in some areas of construction reflected in merchant sales. Slowing demand throughout the final quarter, however, has helped to ease pressures on product supply.

“With forecasts for 2023 predicting further slowdown in the first half of the year, general product availability should have an opportunity to recover before the market begins to recover in the second half.”

Emile van der Ryst, senior client insight manager at Trade at GfK, added: “During 2021, we widely believed that things were on their way up, with various market predictions at the beginning of 2022 indicating some form of growth – but the year turned out completely different.

“A quarterly review against 2021’s applicable quarter shows the increased difficulty the sector experienced as the year went on. The first quarter saw value growth of +17.7%, followed by +4.1%, +4.3% and +2.9% in quarters two to four. Price growth was consistently high each quarter, sitting between +15.0% and +17.7%, while volume started at +1.5% in quarter one and dropped to -11.6% in the fourth quarter.”

{kind=link}