Recent years have seen an increase in the construction of high-rise, with more high-rise buildings being constructed than at any other time.

Recent years have seen an increase in the construction of high-rise, with more high-rise buildings being constructed than at any other time.

Across the UK there are currently over 270 existing high-rise buildings and structures, of which around 70% are in London. There are just 17 high-rise buildings over 150m (492ft.) in height and just one building – The Shard in London – over 300m, and London itself is considered ‘low-rise’ for a global city and financial capital of the world.

However, in recent years, there has been an increase in the number of high-rise buildings proposed and approved for construction in the UK. The UK development pipeline currently stands at around 500 buildings, of which over 85% are planned in London, while the rest are clustered in key cities such as Birmingham, Liverpool, Manchester and Salford.

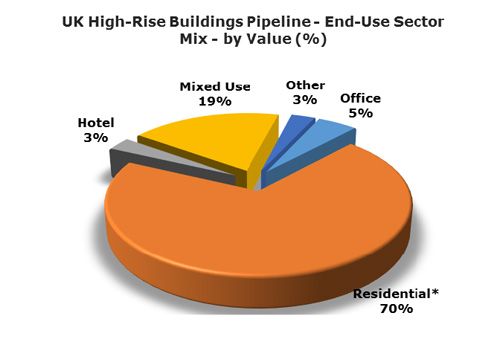

In terms of end-use sector, around 70% of high-rise buildings currently under construction or under consideration across the UK are primarily residential, but with an element of mixed-use, e.g. retail, community or leisure.

AMA Research has revealed that in London, the high-rise market is being driven by the buoyant private housing sector, especially at the top-end of the market, and resurgence in demand for commercial property.

It suggests that the concept of high-rise living has changed and the majority of high-rise residential tower blocks in UK cities are now being developed as luxury accommodation, with a mixed-use element incorporating leisure facilities, concierge services, restaurants and retail.

Such a trend may not necessarily be good for the housing industry, as Hayley Thornley, research manager at AMA Research, explained: “Going forward, the high-rise construction market is set to continue to grow, with the ever-increasing demand for housing.

“However, there are concerns about too many projects aimed at the luxury end of the market, which is not matched with housing demand. In addition, the uncertainties surrounding the EU referendum may influence some high-rise schemes, with many projects in the pipeline forecast to exceed stated completion dates.”

The proportion of mixed-use schemes in the high-rise buildings pipeline is set to grow, with around 18% of developments either under construction or proposed with a mixed-use function. In the office market, rising take-up, low availability of grade-A space and increasing rents in cities such as Manchester, Bristol, Birmingham, Leeds and Edinburgh, is helping to boost output in the commercial office sector and has led to more speculative building.

Sustained growth in the private rented sector (PRS) is also driving the development of high-rise housing, with increasing financial backing from both domestic and foreign institutional investors. Student accommodation also forms a small, but significant proportion of high-rise building development with a number of schemes currently in planning.

Key factors affecting the development of high-rise buildings include cost, space efficiency, wind & seismic considerations, structural safety, risk challenges both on site and in completed buildings, speed of elevators, new building materials to potentially replace steel and concrete and damping systems. In addition, significant technical and logistical factors include pumping and placing concrete at extreme heights, and craning and lifting items to extreme heights.

The definition of high-rise buildings varies, but in this report AMA Research looks at UK regional and London developments of 15-20 storeys and above.

The ‘Construction in the High-Rise Buildings Market Report – UK 2016-2020 Analysis’ report is published by AMA Research and can be ordered online at www.amaresearch.co.uk.