The latest UK Construction PMI data has pointed to the fasted increase in new work for seven months, which has aided a continued rise in the country’s construction output.

However, this has been met with business optimism dropping to a 17-month low, with rising inflation and concerns about the economic impact of the war in Ukraine. While around 48% of the survey panel expected a rise in business activity during the year ahead, and only 15% predict a decline, the balance of positive sentiment was the weakest seen since October 2020.

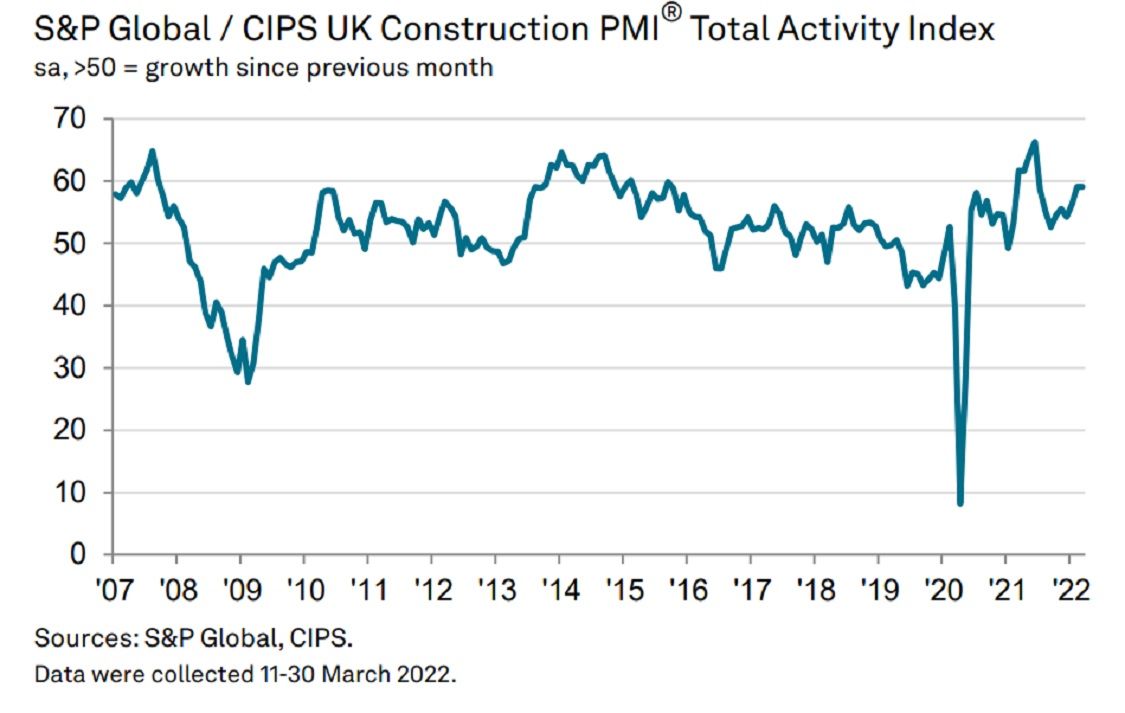

Index

The headline S&P Global / CIPS UK Construction Purchasing Managers’ Index registered 59.1 in March, unchanged from February and well above the 50.0 mark that separates expansion from contraction. The latest reading signalled the joint-fastest rate of output growth since June 2021.

Commercial work was the best-performing segment in March (60.8), with projects restarting amid the roll back of pandemic restrictions. This part of the construction sector has seen output growth accelerate for three months in a row and the latest upturn was the strongest since June 2021.

In contrast, the recoveries in civil engineering (56.3) and residential work (54.9) lost momentum in March. The latter saw the slowest expansion of the three broad categories monitored by the survey.

Total new orders expanded at a robust and accelerated pace in March, with the latest rise the strongest since August 2021. Construction companies typically cited improving tender opportunities and resilient customer demand, despite some reports that economic uncertainty and rising costs had limited new business growth.

Job creation and purchasing

Rising workloads contributed to a considerable rise in staffing numbers during March. However, the pace of job creation eased to its weakest so far this year amid ongoing difficulties filling vacancies.

Mirroring the trend for new orders, the latest data signalled a sharper increase in purchasing activity across the construction sector. Input buying rose at the steepest pace since July 2021, driven by a combination of stronger demand and efforts to build stocks where possible.

Supply issues

Capacity constraints, a lack of haulage availability and ongoing logistics difficulties led to another sharp downturn in supplier performance. Around 33% of the survey panel reported longer lead times for construction products and materials, while only 1% saw an improvement. However, delays remained less widespread than the peak seen last summer.

Imbalanced supply and demand, alongside escalating energy, fuel and commodity prices, resulted in a rapid rise in average cost burdens in March. The overall rate of input price inflation accelerated sharply since February and was the highest for six months.

Industry thoughts…

Joe Sullivan, partner at MHA, believes the country’s relentless housing boom and easing supply chain issues are driving cautious optimism across the sector, despite the impact of inflation and the ongoing war in Ukraine.

He said: “The UK housing sector’s continued growth in March has underpinned another fine month for the construction industry. Demand for new build homes shows no sign of abating, fuelled by mortgages remaining comparatively cheap (despite the recent base rate increase from the Bank of England). While material and labour shortages could prove potential bumps in the road ahead, the outlook for the residential sector remains very rosy.

“Sector confidence has also been boosted by some easing of supply chain issues so far this year, however the ongoing war in Ukraine is expected to put this in jeopardy. The true impact of the war and resulting sanctions on Russia will take time to materialise and as such, certain supply chains must swiftly pivot towards other sources for their materials. The Forest Stewardship Council (FSC)’s decision to remove certification of timber originating from Russia and Belarus is a prime example of the war’s impact on the sector, with architects and contractors set to face obstacles in delivering jobs on time and to specification.

“The recent Spring Statement was a golden opportunity to embolden the sector against such uncertainties. Instead, construction businesses were underwhelmed by the Chancellor’s scant announcements. A reduction in VAT on home energy efficiency products such as solar energy systems is welcome in the long run, but is highly unlikely to force hard pressed consumers to shell out now and it’s an insipid stride in the UK’s path to achieve net zero.

“What’s more, Rishi Sunak’s decision to abolish the sector’s red diesel rebate appears illogical in the current climate, making the rise in energy costs even more acute. Whilst the 5p reduction in fuel duty mitigates the cost increase construction firms will face, the switch to white diesel on top of other inflationary pressures will heighten concern that weaker companies will fail.

“Construction businesses will now be eyeing the Autumn Budget with anticipation for greater support, particularly following The Chancellor’s intention to invest in training and revaluate the effectiveness of the apprenticeship levy. Greater attention must now be paid to ensure that job vacancies are reduced, and skillsets are future proofed towards building an energy efficient and sustainable future, of which policy makers must agree.”

>>Read more PMI data coverage here.

{kind=link}