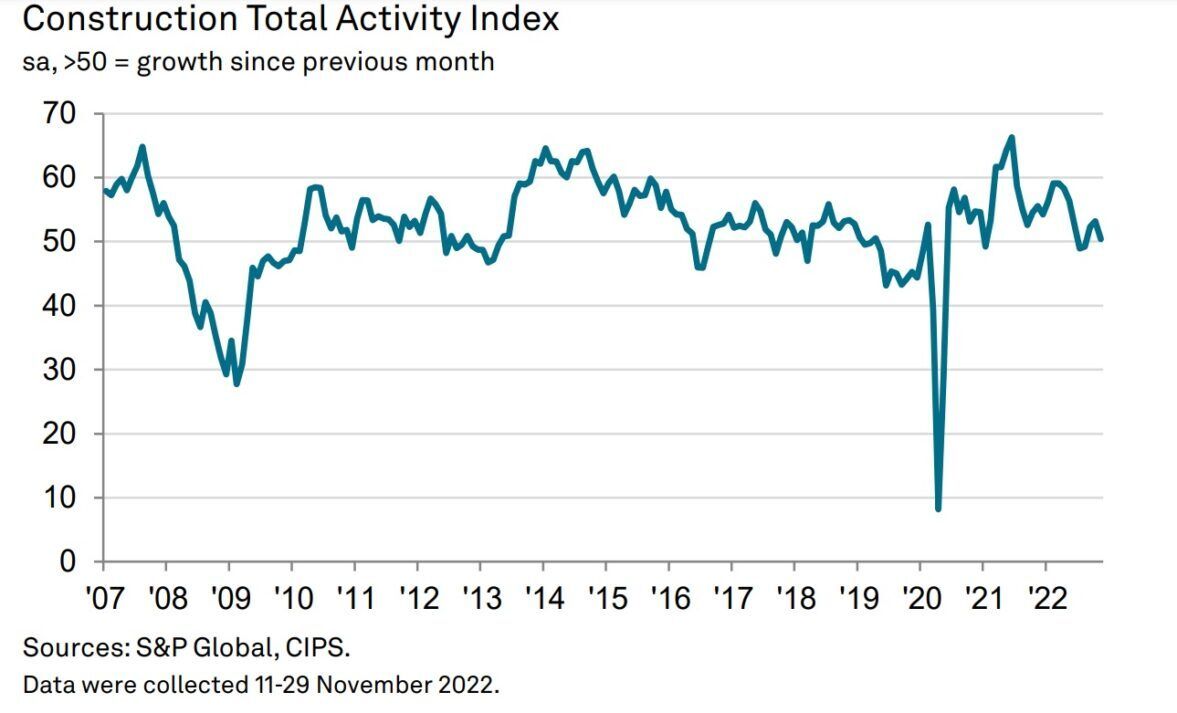

UK construction companies signalled a renewed slowdown in business activity growth during November, reflecting subdued demand and reduced risk appetite among clients with the latest reports noting that borrowing costs and worries about the economic outlook had curtailed the activity.

At 50.4 in November, the headline seasonally adjusted S&P Global / CIPS UK Construction Purchasing Managers’ Index (PMI) registered above the 50.0 no-change mark for the third month running. However, the index was down from 53.2 in October and pointed to the weakest performance since August.

Falling optimism

Moreover, expectations for business activity growth during the year ahead continued to slide in November, with optimism the lowest for two-and-a-half years as around only 29% of the survey panel anticipates a rise in business activity in 12 months’ time, while 26% forecast a decline. Aside from the levels seen at the start of the pandemic, the degree of positive sentiment was the joint-weakest since December 2008.

Anecdotal evidence suggested that recession worries, higher interest rates and a subdued housing market outlook had all weighed on optimism.

Activity

Commercial work was the only segment to register an overall rise in business activity in November (index at 51.1). House building activity meanwhile stalled (index at 50.0), which ended at three-month period of marginal expansion. Construction companies often noted higher mortgage rates and falling consumer confidence as factors that had held back residential activity.

Meanwhile, civil engineering activity (46.7) declined for the fifth consecutive month. The latest reduction was the sharpest since August. Lower volumes of output were mainly linked to a lack of new work to replace completed projects.

November data pointed to modest increase in total new orders across the construction sector, which contrasted with a slight decline in October. However, the rise in new business intakes was much weaker than seen on average in the first half of 2022. Survey respondents often noted that weaker domestic economic conditions had acted as a headwind to client spending.

Job creation

Employment numbers continued to increase in November, but the rate of job creation eased to its slowest since February 2021. Construction companies suggested that concerns about rising costs and weaker growth had led to more cautious hiring policies.

In contrast to the slowdown in staff recruitment, latest data signalled the fastest increase in input buying since July. Higher levels of purchasing activity were linked to rising workloads and improved raw material availability, although some cited efforts to place orders ahead of supplier prices hikes.

Inflation

Average cost burdens increased sharply in November, which was linked to rising energy prices, tight supply conditions and general inflationary pressures. However, the overall rate of input cost inflation eased to its least marked since January 2021, partly due to softer commodity prices. Meanwhile, suppliers’ delivery times lengthened to the greatest extent since July. Survey respondents suggested that transport and logistics delays had led to longer wait times for the receipt of construction products and materials.

{kind=link}